🌙 Welcome to Tekin Night May 30, 2026

Good evening, tech enthusiasts! Tonight we're diving deep into six major stories that are reshaping the technology landscape. From Amazon's aggressive satellite deployment to Bitcoin's historic ETF crisis, from Google's rapid response to user feedback to Apple's most expensive camera upgrade ever—we've got comprehensive analysis and strategic insights you won't find anywhere else.

⚡ Tonight's Headlines:

🚀 Atlas V Deploys 29 Amazon Leo Satellites in Starlink Challenge

💸 Bitcoin ETFs Hemorrhage $2.8B in Record Nine-Day Outflow Streak

🤖 Google Rapidly Adjusts Gemini Usage Limits After User Backlash

📸 iPhone 18 Pro Variable Aperture Camera Costs Apple 50% More

🎮 Xbox Showcase Will Skip Project Helix Next-Gen Console News

📉 Crypto-Stock Divergence Reaches Sharpest Level of 2026

🌌 Buckle up for deep-dive analysis, strategic insights, and forward-looking predictions!

🚀 Atlas V Success: Amazon Leo Takes Major Step Toward Starlink Competition

United Launch Alliance's Atlas V rocket successfully deployed 29 Amazon Leo internet satellites to orbit at 7:53 PM EDT on May 29, 2026, from Launch Complex 41 at Cape Canaveral Space Force Station. This marks the seventh production batch for Amazon in 2026 and represents a critical milestone in the company's ambitious plan to challenge SpaceX's Starlink dominance in the satellite internet market.

The mission, designated Leo 7, utilized the powerful Atlas V 551 configuration—equipped with five solid rocket boosters that provide exceptional lift capacity. Amazon is constructing a 3,236-satellite constellation designed to deliver high-speed internet to underserved regions globally. However, the company faces a formidable challenge: under its federal license, Amazon must activate half of this network by July 30, 2026—just two months away.

This deadline isn't arbitrary—it's a regulatory requirement from the Federal Communications Commission (FCC) designed to prevent spectrum hoarding. Companies that fail to meet deployment milestones risk losing their orbital slots and spectrum allocations. With approximately 200+ satellites currently in orbit, Amazon needs to accelerate deployment dramatically to reach the 1,618-satellite threshold by late July. This explains the aggressive launch cadence we're witnessing in 2026.

📊 Leo 7 Mission Critical Statistics

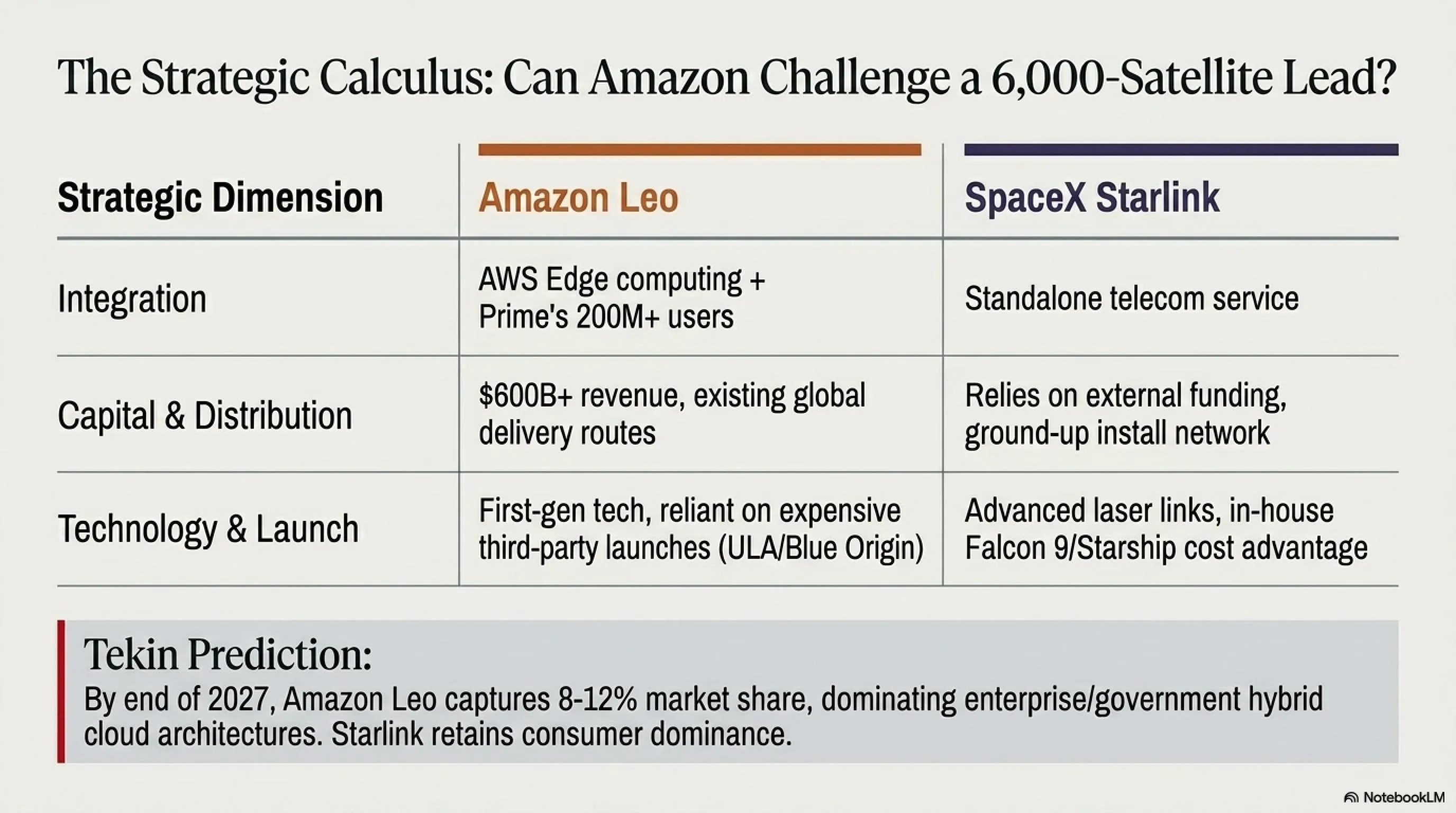

The strategic importance of this launch cannot be overstated. Amazon is entering a market dominated by Starlink, which has over 6,000 operational satellites and serves millions of customers across 70+ countries. SpaceX's head start of nearly five years gives it enormous advantages in technology maturity, customer acquisition, and operational experience. However, Amazon brings formidable assets to this competition that could reshape the satellite internet landscape.

First, Amazon's integration with AWS (Amazon Web Services) creates unique synergies. The company can offer bundled services combining satellite internet with cloud computing, edge computing, and content delivery networks—something Starlink cannot match. For enterprise customers, this integration could be transformative, enabling hybrid cloud architectures that seamlessly blend terrestrial and satellite connectivity.

Second, Amazon's financial resources are virtually unlimited. With a market capitalization exceeding $2 trillion and annual revenue surpassing $600 billion, the company can sustain years of losses to capture market share. This is the same playbook Amazon used to dominate e-commerce and cloud computing—aggressive pricing, massive infrastructure investment, and patient capital.

🔍 Tekin Analysis: Can Amazon Actually Challenge Starlink's Dominance?

The conventional wisdom suggests Starlink's lead is insurmountable. However, our analysis reveals several strategic advantages that could enable Amazon to capture significant market share:

✅ Amazon's Strategic Advantages:

- AWS Integration: Amazon can bundle satellite internet with AWS services, creating a comprehensive solution for enterprise customers. Imagine edge computing nodes connected via Leo satellites, enabling real-time data processing in remote locations. This is a $50B+ market opportunity that Starlink cannot address.

- Prime Ecosystem: With 200+ million Prime members globally, Amazon has a built-in customer base. Offering Leo internet as a Prime benefit could drive rapid adoption, especially in rural areas where Prime delivery is already popular.

- Logistics Network: Amazon's unparalleled distribution infrastructure enables rapid equipment deployment. The company can leverage existing delivery routes to install customer terminals, reducing installation costs and time.

- Aggressive Pricing: Amazon has a proven track record of using predatory pricing to eliminate competitors. The company can afford to operate Leo at a loss for years, subsidizing service costs to gain market share—exactly what it did with AWS in the early 2010s.

- Government Contracts: Amazon's experience with government cloud contracts (AWS GovCloud) positions it well for lucrative military and government satellite internet contracts, a market worth billions annually.

❌ Challenges Amazon Must Overcome:

- Technology Gap: Starlink's satellites are more advanced, with inter-satellite laser links enabling global coverage without ground stations. Amazon's first-generation satellites lack this capability, limiting performance.

- Launch Capacity Constraints: SpaceX controls its own launch infrastructure with Falcon 9 and Starship, enabling rapid, cost-effective deployment. Amazon relies on third-party providers (ULA, Blue Origin), which are more expensive and less frequent.

- Brand Perception: Amazon is known for e-commerce and cloud computing, not telecommunications. Building trust in a new market segment requires significant marketing investment and time.

- Regulatory Hurdles: The FCC's July 2026 deadline creates immense pressure. Missing this milestone could result in spectrum forfeiture, setting the project back years.

- Operational Complexity: Running a satellite constellation requires expertise in orbital mechanics, RF engineering, and network operations—domains where Amazon has limited experience.

💡 Tekin Prediction: By end of 2026, Amazon Leo will capture 8-12% of the satellite internet market, primarily in enterprise and government segments. The real competition begins in 2027 when both constellations are fully operational. We expect a price war that will benefit consumers but squeeze margins for both companies. Long-term winner: whoever integrates satellite internet most effectively with adjacent services (AWS for Amazon, Starship for SpaceX).

🌍 Global Impact: The satellite internet market is projected to reach $30 billion annually by 2030. Amazon's entry intensifies competition, which will drive down prices and improve service quality. Rural and underserved communities worldwide stand to benefit most, gaining access to high-speed internet that was previously unavailable or prohibitively expensive. This democratization of connectivity could unlock trillions in economic value.

💸 Bitcoin ETF Crisis: $2.8B Hemorrhage in Historic Nine-Day Outflow Streak

U.S. spot Bitcoin ETFs recorded their longest outflow streak in history—nine consecutive trading days from May 14-29, 2026—with investors withdrawing approximately $2.8 billion from these products. This unprecedented capital flight occurred while the S&P 500 posted its ninth consecutive week of gains, reaching a record high of 7,592. The divergence between traditional equities and cryptocurrency markets has reached its sharpest level in 2026, signaling a fundamental shift in institutional investor sentiment.

Bitcoin fell 2.6% to $73,445 during this period, while Ethereum dropped 2.5% to $2,011. Meanwhile, the Nasdaq Composite surged 8% in May alone, driven by explosive gains in AI and semiconductor stocks. Nvidia, AMD, and other AI infrastructure companies posted double-digit returns, attracting capital that might have otherwise flowed into crypto assets. This represents a critical inflection point: institutional investors are choosing between crypto and AI equities, and AI is winning decisively.

📉 Bitcoin ETF Outflow Crisis: By the Numbers

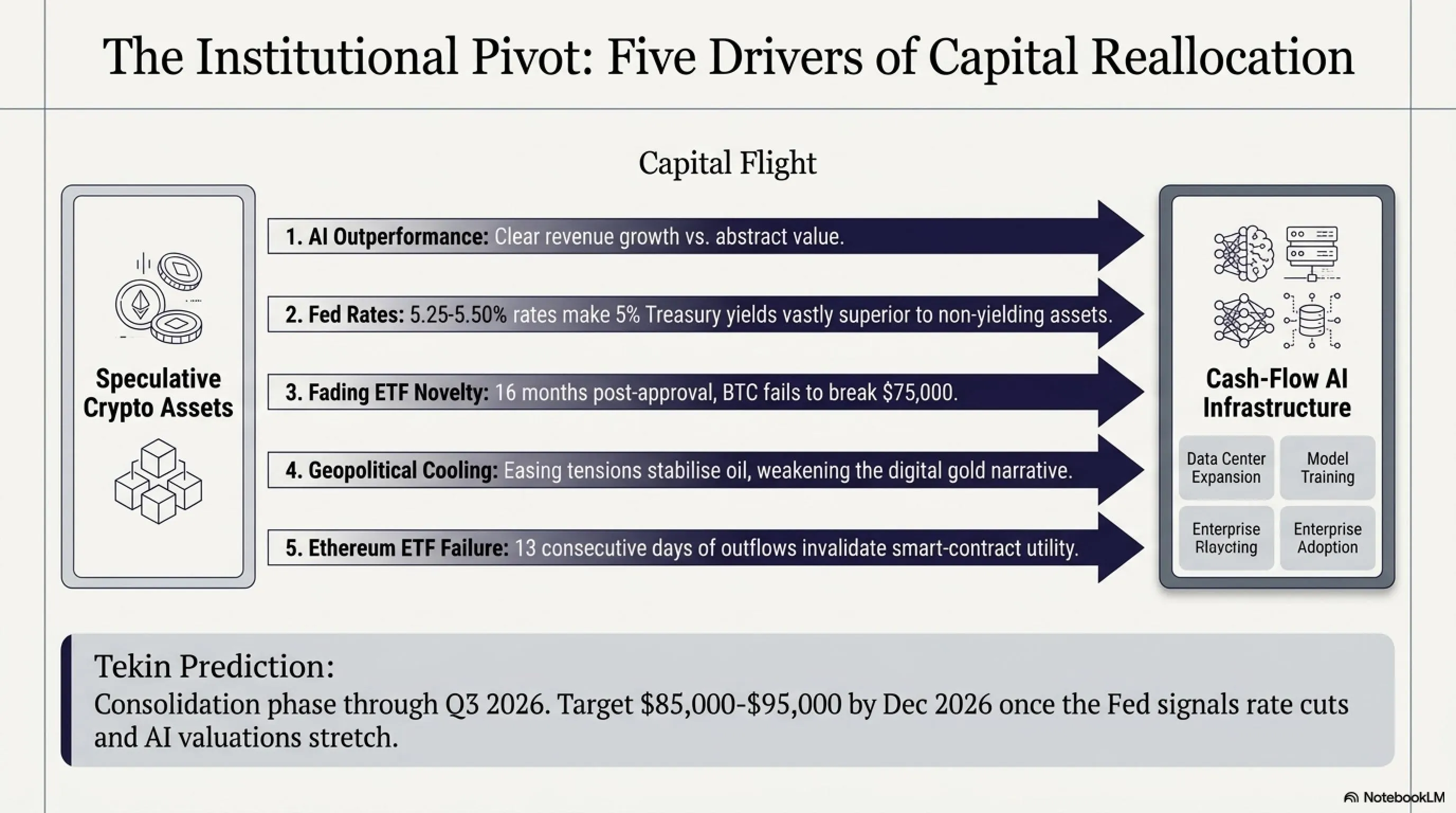

What's driving this historic capital exodus? Our analysis identifies five primary factors, each reflecting deeper structural changes in how institutional investors view digital assets:

🔍 Five Drivers of the Bitcoin ETF Exodus

1️⃣ AI Equity Outperformance

The most significant factor is the explosive performance of AI and semiconductor stocks. Nvidia has gained 45% year-to-date, AMD is up 38%, and smaller AI infrastructure plays like Arista Networks and Marvell Technology have posted even larger gains. Institutional portfolio managers face a stark choice: allocate to Bitcoin with uncertain regulatory status and no cash flows, or invest in profitable AI companies with clear growth trajectories. The data shows they're choosing AI overwhelmingly.

2️⃣ Federal Reserve's Higher-for-Longer Policy

With the Fed maintaining interest rates at 5.25-5.50%, risk-free Treasury yields remain attractive at 4.5-5.0%. For institutional investors with fiduciary responsibilities, the calculus is straightforward: why accept Bitcoin's volatility when you can earn 5% risk-free? This dynamic persists until the Fed signals rate cuts, which may not occur until Q4 2026 or even 2027 if inflation remains sticky.

3️⃣ Cooling ETF Novelty Effect

The initial euphoria surrounding Bitcoin ETF approvals in January 2024 has faded. Early adopters who rushed in during the first months are now reassessing their allocations. Many institutional investors allocated 1-2% of portfolios to Bitcoin ETFs as an experiment; after 16 months of observation, some are concluding the risk-reward profile doesn't justify continued exposure, especially given Bitcoin's failure to break above $75,000 despite ETF approval.

4️⃣ Geopolitical Risk Reduction

Positive developments in U.S.-Iran nuclear negotiations have reduced geopolitical tensions, causing oil prices to stabilize near $92/barrel (down from $105 in March). Bitcoin has historically benefited from geopolitical uncertainty as a "digital gold" safe haven. With tensions easing, this narrative weakens, reducing Bitcoin's appeal to macro hedge funds and geopolitical risk traders.

5️⃣ Ethereum ETF Underperformance

Ethereum ETFs have experienced 13 consecutive days of outflows, even worse than Bitcoin. This suggests broader skepticism about crypto assets as an investment class, not just Bitcoin-specific concerns. The failure of Ethereum—which has a clearer utility narrative through DeFi and smart contracts—to attract sustained institutional interest raises questions about the entire crypto ETF thesis.

🔍 Tekin Analysis: Is This a Crisis or Healthy Consolidation?

Contrary to bearish narratives, we view this outflow streak as healthy market maturation rather than existential crisis. Here's our contrarian take:

✅ Bullish Indicators Being Overlooked:

- Assets Under Management Still Massive: Despite $2.8B in outflows, ETFs still hold $94.25B in Bitcoin—equivalent to ~1.28 million BTC. This represents 6.4% of Bitcoin's total supply, a staggering concentration that provides price support.

- Price Stability: Bitcoin has remained range-bound between $73,000-$75,000 despite massive outflows. This suggests strong underlying demand absorbing ETF selling pressure. In previous cycles, similar outflows would have triggered 20-30% corrections.

- High Trading Volume: Daily ETF trading volume of $2.36B indicates robust liquidity and continued institutional engagement. Low volume would be concerning; high volume during outflows suggests active rebalancing, not panic selling.

- Institutional Infrastructure Intact: Major institutions like BlackRock, Fidelity, and Ark Invest remain committed to their Bitcoin ETF products. No provider has exited the market, indicating long-term confidence despite short-term headwinds.

- Retail Accumulation: On-chain data shows retail wallets (< 1 BTC) have been accumulating during this period, suggesting smart money is buying the dip while institutions rotate to AI stocks.

⚠️ Legitimate Concerns:

- Narrative Weakness: Bitcoin lacks a compelling growth narrative in 2026. "Digital gold" isn't resonating when gold itself is underperforming. "Inflation hedge" rings hollow with inflation moderating. The halving in April 2024 hasn't produced the expected price surge.

- Competition from AI: The AI investment thesis is clearer and more compelling. Institutional allocators have limited risk budgets; if they're allocating to high-risk, high-reward assets, AI equities offer better risk-adjusted returns than crypto.

- Regulatory Uncertainty: Despite ETF approval, broader crypto regulation remains unclear. The SEC's ongoing enforcement actions against exchanges and DeFi protocols create uncertainty that institutional investors dislike.

- Lack of Catalysts: What drives Bitcoin to $100,000+? ETF approval was supposed to be the catalyst, but it's proven insufficient. Without new catalysts (Fed rate cuts, major corporate adoption, regulatory clarity), Bitcoin may remain range-bound.

💡 Tekin Prediction: This consolidation phase extends through Q3 2026. Bitcoin trades between $70,000-$78,000 as institutional flows remain muted. The turning point comes in Q4 2026 when: (1) Fed signals rate cuts for 2027, (2) AI stock valuations become stretched, prompting rotation, and (3) Bitcoin's supply shock from the 2024 halving begins manifesting. Target: $85,000-$95,000 by December 2026, with $100,000+ in Q1 2027. Patient capital will be rewarded.

🤖 Google's Rapid Response: Gemini Usage Limits Adjusted After User Backlash

Google swiftly adjusted Gemini's controversial usage limits after widespread user complaints, demonstrating impressive organizational agility. At Google I/O 2026 last week, the company introduced a new compute-based usage system that replaced simple message counts with a more sophisticated measurement of computational resources consumed. However, implementation issues caused users to hit limits far faster than expected, triggering a wave of criticism from paying Gemini Advanced subscribers.

The new system implemented rolling five-hour windows plus weekly caps, designed to prevent abuse while allowing legitimate heavy usage. In theory, this approach makes sense—complex requests involving video analysis, code generation, or multi-modal reasoning consume vastly more computational resources than simple text queries. However, users reported exhausting their entire five-hour quota with just one or two complex requests, particularly when using Gemini Omni for video analysis. This created a frustrating experience where paying customers couldn't use the service they'd purchased.

🔧 Gemini Usage Limit Changes (May 28-29, 2026)

- Per-Prompt Consumption Cap: Individual requests now cannot consume more than a specified percentage of your quota, preventing single queries from exhausting your entire allocation. This addresses the primary complaint where one video analysis request would drain the entire five-hour window.

- Failed Requests Don't Count: If your request encounters an error or fails to complete, it no longer deducts from your quota. This is crucial for developers and power users who iterate rapidly and encounter frequent errors during experimentation.

- Flash-Lite Now Unlimited: Google's lightweight Gemini Flash-Lite model is now available without quota restrictions, providing a fallback option for users who hit limits on more powerful models. This is particularly useful for simple queries that don't require full Gemini Pro capabilities.

- Detailed Usage Visibility: Users can now see exactly how much quota each request consumed, enabling better understanding and optimization of usage patterns. Transparency was a major complaint; this addresses it directly.

- Omni Bug Fixed: A critical bug causing Gemini Omni video requests to consume disproportionate quota has been resolved. This was the most egregious issue, where a single 2-minute video analysis could exhaust an entire day's quota.

These changes demonstrate Google's responsiveness to user feedback, but they also reveal deeper issues in how the company approaches product launches. With 900 million monthly active users, Gemini is one of the world's largest AI platforms, competing directly with ChatGPT and Claude. Google cannot afford to alienate paying customers, especially when competitors are aggressively courting dissatisfied users with promotional offers and feature improvements.

🔍 Tekin Analysis: Three Critical Product Management Failures

This incident provides a masterclass in what not to do when launching major product changes. Google made three fundamental errors:

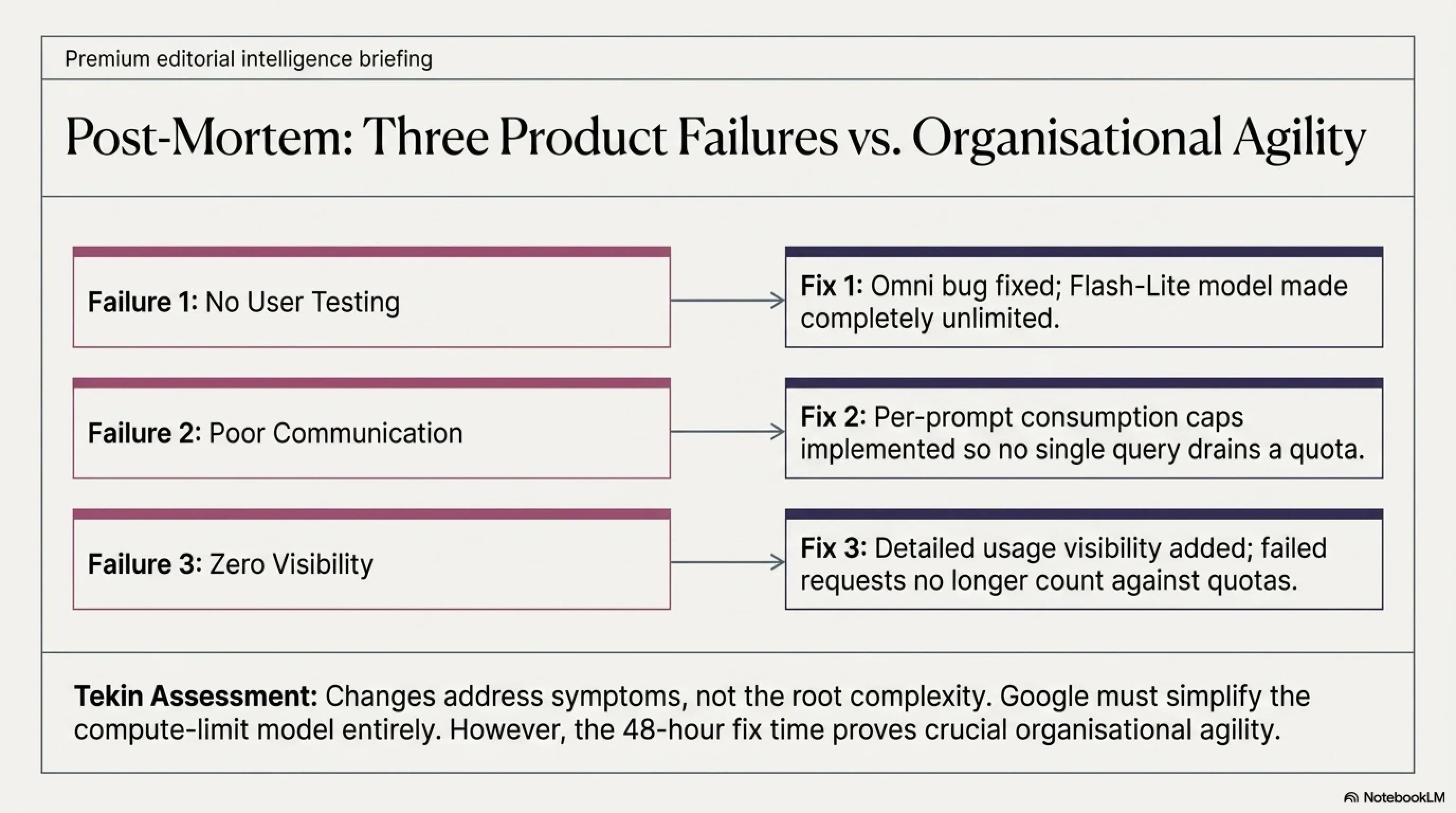

❌ Failure #1: Insufficient Testing with Real Users

Google deployed the compute-based system to all users simultaneously without adequate beta testing. A proper rollout would have involved: (1) internal dogfooding for 2-3 weeks, (2) limited beta with 10,000-50,000 users for 1-2 weeks, (3) gradual rollout to 10%, 25%, 50%, then 100% of users over 2-3 weeks. This staged approach would have surfaced the Omni bug and quota exhaustion issues before they affected millions. Instead, Google treated 900 million users as beta testers, damaging trust and brand reputation.

❌ Failure #2: Poor Communication and Education

Users didn't understand what "compute-based usage" meant or why their quotas were exhausting so quickly. Google should have provided: (1) clear documentation explaining the new system with examples, (2) in-app notifications warning users before they hit limits, (3) educational content showing how to optimize usage, (4) comparison tools showing how different request types consume quota. The lack of communication created confusion and frustration that could have been avoided with better user education.

❌ Failure #3: No Visibility or Control

Users had no way to see their current quota consumption, predict when they'd hit limits, or understand which requests were expensive. This lack of transparency is unacceptable for a paid service. Imagine if your phone carrier didn't show data usage until you hit your cap—that's essentially what Google did. The company should have launched with: (1) real-time quota dashboard, (2) per-request cost estimates before submission, (3) usage alerts at 50%, 75%, and 90% of quota, (4) ability to purchase additional quota for heavy users.

✅ Silver Lining: Google's response time was impressive—changes implemented within 48 hours of widespread complaints. This demonstrates that the Gemini team is agile, customer-focused, and empowered to make rapid decisions. In contrast, many large tech companies would have taken weeks or months to respond. The speed of Google's response partially mitigates the initial failure and shows organizational maturity.

🎯 Competitive Context: This incident occurs as competition in the AI assistant market intensifies. ChatGPT recently announced GPT-5.5 with improved reasoning, Claude introduced extended context windows up to 500K tokens, and Microsoft's Copilot is gaining enterprise traction. Google cannot afford missteps that drive users to competitors. The rapid response suggests Google understands the stakes—in AI, user loyalty is fragile and switching costs are near zero.

📸 iPhone 18 Pro Camera: Apple's Most Expensive Upgrade Yet

Renowned Apple analyst Ming-Chi Kuo revealed that the variable aperture camera system coming to iPhone 18 Pro models will cost Apple 50% more than current camera units—marking the most significant camera investment in the Pro line's history. This isn't just an incremental upgrade; it represents Apple's commitment to maintaining camera leadership in an increasingly competitive smartphone market.

Variable aperture technology allows the lens to physically adjust its opening size, similar to professional DSLR cameras. This enables precise control over depth of field, light intake, and image quality across diverse shooting conditions. Samsung pioneered this feature in smartphones with the Galaxy S9 in 2018, but Apple is now implementing it with characteristic attention to detail and integration with computational photography.

📊 iPhone 18 Pro Camera Specifications

According to Kuo's supply chain sources, production began in early 2026, with Sunny Optical supplying 40-50% of the variable aperture units. The 50% cost premium reflects the mechanical complexity of the system—moving parts require precision engineering, quality control, and durability testing that fixed-aperture lenses don't need. Additionally, Apple is transitioning the ultra-wide camera from flip-chip to chip-on-board technology, which improves image quality while reducing costs.

🔍 Tekin Analysis: Strategic Rationale Behind Apple's Expensive Camera Bet

Why is Apple willing to absorb a 50% cost increase for this camera upgrade? Our analysis reveals a multi-layered strategic rationale:

✅ Why Variable Aperture Makes Strategic Sense:

- Differentiation from Android: Most Android flagships have converged on similar camera specs. Variable aperture provides a tangible, demonstrable advantage that Apple can market effectively. Consumers understand "professional camera control" even if they don't understand the technical details.

- Justifies Pro Pricing: The gap between iPhone standard and Pro models has narrowed in recent years. Variable aperture creates clear differentiation, justifying the $200-300 premium for Pro models. This protects Apple's high-margin product mix.

- Computational Photography Synergy: Variable aperture combined with Apple's advanced computational photography creates capabilities impossible with fixed aperture. Real-time depth-of-field adjustment, adaptive low-light performance, and professional-grade bokeh become possible.

- Professional Market Expansion: Apple is targeting professional photographers and videographers who currently carry dedicated cameras. If iPhone 18 Pro can replace a $2,000 mirrorless camera for many use cases, the value proposition becomes compelling.

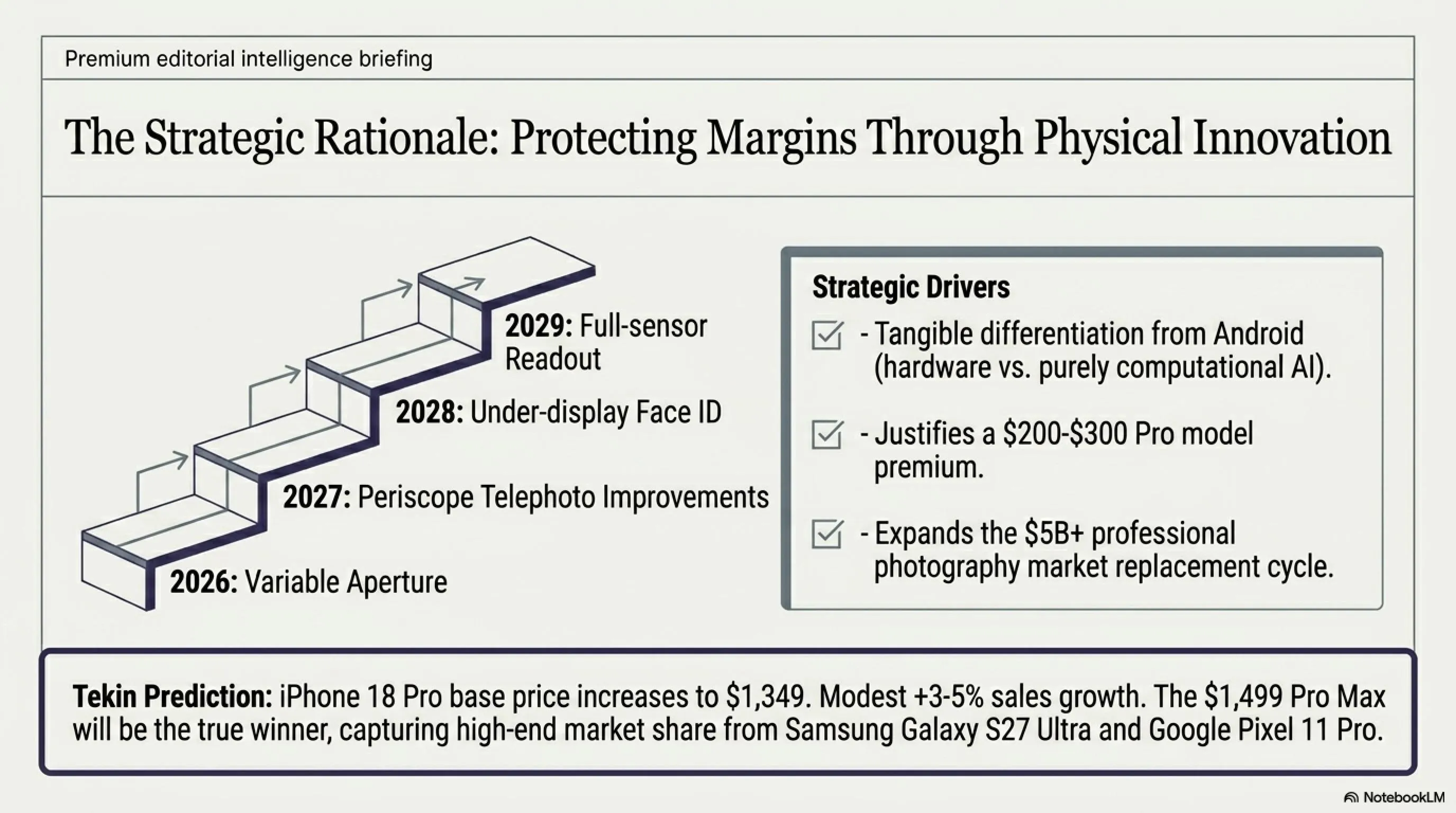

- Long-term Platform Play: This is the first step in Apple's four-phase camera upgrade roadmap. Variable aperture in 2026, followed by periscope telephoto improvements in 2027, under-display Face ID in 2028, and full-sensor readout in 2029. Each phase builds on the previous, creating sustained differentiation.

❌ Risks and Challenges:

- Price Increase Likely: A 50% camera cost increase translates to $150-200 higher retail price for iPhone 18 Pro. At $1,349-1,399, the Pro models risk pricing out mainstream consumers, limiting addressable market.

- Mechanical Complexity: Moving parts introduce failure points. If variable aperture mechanisms fail at higher rates than fixed lenses, warranty costs and customer satisfaction could suffer. Apple's reputation for reliability is at stake.

- Late to Market: Samsung introduced variable aperture in 2018 but abandoned it in later models due to reliability concerns and limited consumer appreciation. Apple is betting it can succeed where Samsung struggled—a risky assumption.

- User Education Required: Most consumers don't understand aperture, depth of field, or f-stops. Apple must invest heavily in marketing and education to help users appreciate the feature. Without proper education, the upgrade may not drive purchase decisions.

- Diminishing Returns: iPhone cameras are already excellent. The improvement from variable aperture may be noticeable to professionals but imperceptible to average users. If consumers can't see the difference, they won't pay the premium.

💡 Tekin Prediction: iPhone 18 Pro starts at $1,349 (up from $1,199), with the variable aperture camera as the headline feature. Initial reviews will be positive, praising image quality improvements. However, sales growth will be modest (+3-5% vs iPhone 17 Pro) as the price increase offsets feature appeal. The real winner: iPhone 18 Pro Max at $1,499, which will capture high-end market share from Android flagships. Long-term, this positions Apple to dominate the professional mobile photography market worth $5B+ annually.

🎮 Xbox Strategy Shift: No Project Helix News at June Showcase

Matt Booty, Xbox's Chief Content Officer, confirmed on the Official Xbox Podcast that the Xbox Games Showcase on June 7, 2026, will not include any announcements about Project Helix, the next-generation Xbox console. His statement was unambiguous: "We want to make the right decisions for the long term, not fast decisions. And I can also say that there won't be Helix news. So Helix will not be in this Showcase."

This decision reflects Microsoft's fundamental strategic pivot away from hardware-centric competition toward a platform-agnostic gaming ecosystem. While Sony prepares PS6 and Valve develops next-generation Steam Machine hardware, Xbox is doubling down on Game Pass and cloud gaming as the future of the platform. The Showcase will focus exclusively on games, with confirmed appearances from Fable (delayed to February 2027), Halo: Campaign Evolved, and Gears of War: E-Day.

🎮 Confirmed Games for Xbox Games Showcase 2026

- Fable: Delayed to February 2027, but new gameplay trailer and deep dive into the reimagined Albion world. Playground Games promises the most ambitious RPG in Xbox history, with dynamic seasons, branching narratives, and next-gen character interactions.

- Halo: Campaign Evolved: Master Chief returns in a campaign-focused experience built on the new Slipspace 2.0 engine. 343 Industries promises a return to Halo's roots with large-scale battles, exploration, and a story that addresses fan criticisms of Infinite.

- Gears of War: E-Day: A dedicated Xbox Direct immediately following the Showcase will provide an extended look at this prequel exploring Emergence Day. The Coalition is leveraging Unreal Engine 5.4 for unprecedented visual fidelity.

- Third-Party Multiplatform Games: Booty confirmed that games releasing on competing platforms will display PlayStation and Nintendo logos alongside Xbox. This transparency reflects Microsoft's new platform-agnostic strategy.

- Surprise Announcements: Industry insiders suggest at least 2-3 unannounced titles from Xbox Game Studios, potentially including Perfect Dark gameplay reveal and a new IP from Obsidian Entertainment.

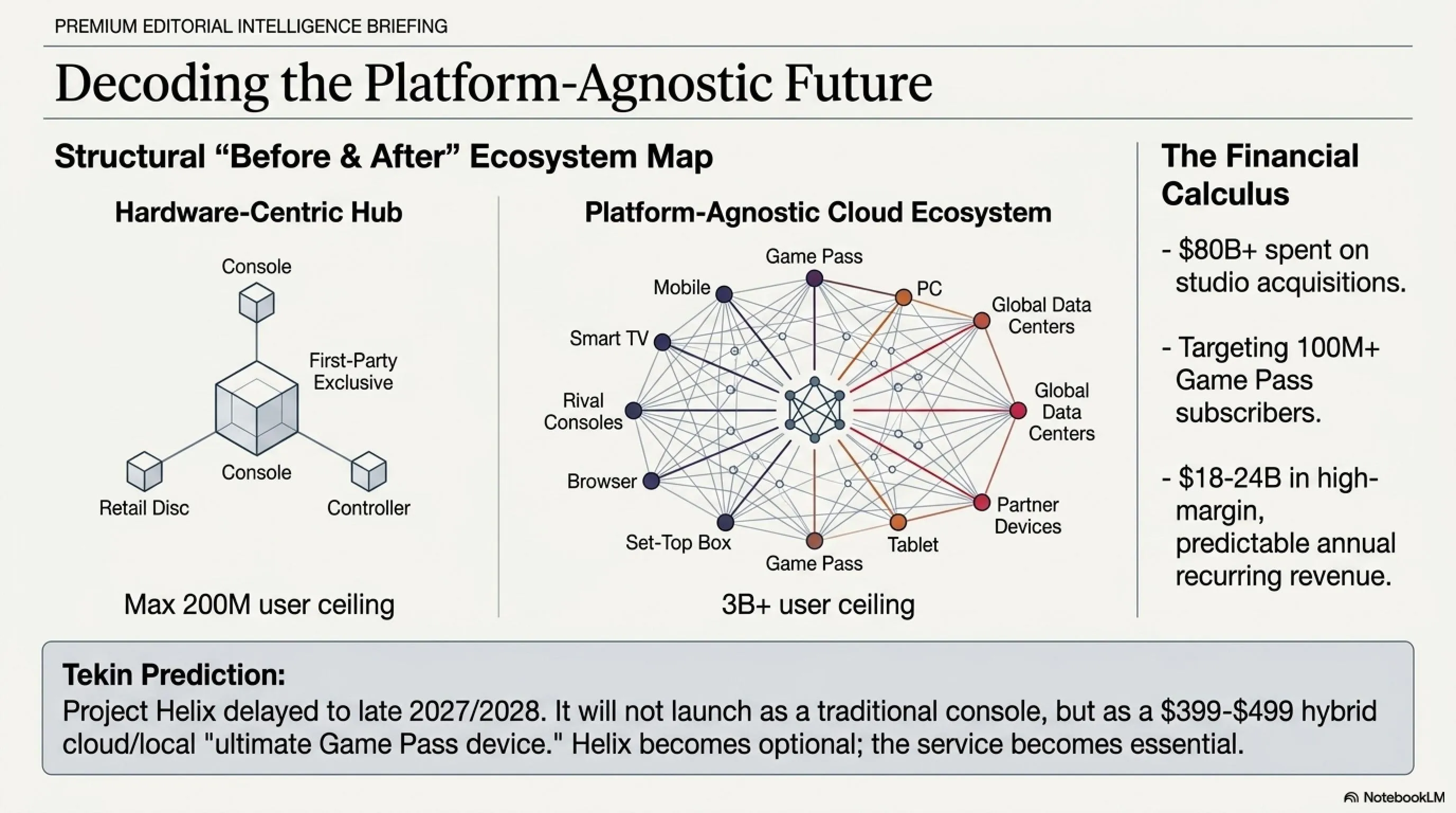

🔍 Tekin Analysis: Decoding Xbox's Platform-Agnostic Future

The Project Helix delay isn't a setback—it's a strategic choice that reveals Microsoft's vision for gaming's future. Let's decode the strategy:

🎯 The New Xbox Strategy: Platform-Agnostic Gaming

Microsoft is executing a multi-year transformation from console manufacturer to gaming platform provider:

- Game Pass Everywhere: The goal is 100+ million Game Pass subscribers across Xbox, PC, mobile, and eventually PlayStation/Nintendo. At $15-20/month, this generates $18-24B annually—far more profitable than console hardware sales.

- Cloud Gaming Priority: Xbox Cloud Gaming (xCloud) enables Game Pass on any device with a screen and internet connection. This eliminates the need for expensive hardware, expanding addressable market from 200M console gamers to 3B+ global gamers.

- Studio Acquisition Over Hardware: Microsoft has spent $80B+ acquiring Activision Blizzard, Bethesda, and other studios. These content assets generate revenue across all platforms, not just Xbox hardware. Call of Duty on PlayStation generates more revenue than Xbox console sales.

- Netflix Model for Gaming: Just as Netflix doesn't manufacture TVs, Xbox doesn't need to manufacture consoles. The value is in the content library and subscription service, not the hardware. Project Helix becomes optional—a premium way to experience Game Pass, not a requirement.

✅ Strategic Advantages:

- Massive Market Expansion: Console gaming is ~200M users. Mobile gaming is 3B+ users. By going platform-agnostic, Xbox can 10x its addressable market.

- Recurring Revenue: Subscription revenue is predictable and high-margin. Hardware sales are lumpy and low-margin. Wall Street values recurring revenue at 5-10x higher multiples.

- Reduced Hardware Risk: Console development costs billions and takes 5-7 years. If Project Helix fails, Microsoft loses years and billions. By delaying, they reduce risk while building the Game Pass ecosystem.

- Competitive Judo: Sony and Nintendo are locked into hardware cycles. Microsoft can compete on software and services where it has advantages (Azure cloud infrastructure, enterprise relationships, financial resources).

❌ Risks and Challenges:

- Brand Identity Erosion: Xbox is synonymous with console gaming. Becoming platform-agnostic risks diluting brand identity and alienating core fans who value the console experience.

- Current Console Sales Decline: Announcing no Helix news accelerates Xbox Series X/S sales decline. Why buy an Xbox when Microsoft is signaling consoles aren't the future?

- Dependency on Competitors: If Game Pass depends on PlayStation and Nintendo allowing it on their platforms, Microsoft cedes control to competitors who can change terms or block access.

- Cloud Gaming Limitations: Latency, bandwidth requirements, and data caps limit cloud gaming adoption. Until these issues are solved, cloud can't fully replace local hardware.

- Execution Risk: This strategy requires flawless execution across cloud infrastructure, content acquisition, and platform partnerships. Any misstep could leave Xbox without a clear market position.

💡 Tekin Prediction: Project Helix launches in late 2027 or early 2028, positioned as "the ultimate Game Pass device" rather than a traditional console. It will be a hybrid cloud/local gaming device, priced at $399-499, with seamless switching between local and cloud gaming. By then, Game Pass will have 75-100M subscribers across all platforms, making Helix optional rather than essential. Microsoft wins by making Xbox a service, not a box.

✅ Advantages of New Strategy

- Access to billions of gamers globally

- Predictable subscription revenue stream

- Reduced dependency on hardware cycles

- Leverage Azure cloud infrastructure

- Compete on content, not hardware specs

- Higher profit margins on services

❌ Risks and Challenges

- Loss of Xbox brand identity

- Declining current console sales

- Dependency on competitor platforms

- Cloud gaming technical limitations

- Alienation of hardcore Xbox fans

- Complex multi-platform execution

📊 Mid-Article Synthesis: Five Patterns Shaping Tech's Future

Tonight's six stories reveal five meta-patterns that will define technology's trajectory through 2027:

- 1. Space Infrastructure Democratization: Amazon's aggressive satellite deployment signals that space is no longer SpaceX's exclusive domain. Multiple well-funded competitors (Amazon, OneWeb, Telesat) are building constellations, driving down costs and improving service. By 2030, satellite internet will be as common as fiber, fundamentally changing global connectivity.

- 2. Financial Market Bifurcation: Traditional equities and crypto assets are decoupling. Institutional capital is choosing AI stocks over Bitcoin, reflecting a preference for cash-flow-generating businesses over speculative assets. This bifurcation will persist until crypto develops clearer utility beyond speculation.

- 3. Rapid Iteration Culture: Google's 48-hour response to Gemini complaints demonstrates that agility is now table stakes for tech giants. Companies that can't iterate rapidly based on user feedback will lose to more nimble competitors. The era of annual product cycles is over.

- 4. Hardware Innovation Renaissance: Apple's 50% camera cost increase shows that physical innovation still matters in an AI-dominated landscape. While software and AI capture headlines, hardware differentiation remains crucial for premium positioning and margin protection.

- 5. Platform-Agnostic Future: Xbox's strategy shift from hardware to services reflects a broader industry trend. Success increasingly depends on ecosystem control and recurring revenue, not hardware sales. This pattern will extend beyond gaming to smartphones, PCs, and other devices.

💭 Final Thoughts: Technology at an Inflection Point

May 30, 2026, will be remembered as a day that crystallized several critical transitions in the technology industry. From space to finance, from AI to hardware, from gaming to platforms—every story tonight reflects an industry in flux, searching for sustainable business models and competitive advantages in an increasingly complex landscape.

Amazon's satellite ambitions demonstrate that even the most capital-intensive, technically complex markets can be disrupted by well-funded challengers with adjacent capabilities. The company's AWS integration and logistics network provide unique advantages that Starlink cannot match, suggesting that the satellite internet market will be more competitive and innovative than many predicted.

Bitcoin's ETF outflows remind us that institutional adoption doesn't guarantee sustained demand. When faced with compelling alternatives—AI stocks with clear growth trajectories and cash flows—institutional investors are choosing traditional equities over crypto assets. This doesn't spell doom for Bitcoin, but it does suggest that crypto needs stronger utility narratives beyond "digital gold" to attract sustained institutional capital.

Google's rapid Gemini adjustments showcase organizational agility that belies the company's massive scale. With 900 million users, Google could have taken weeks to respond to complaints. Instead, changes were implemented within 48 hours, demonstrating that large tech companies can still move quickly when properly motivated by competitive pressure.

Apple's camera investment signals continued belief in hardware differentiation despite the AI software revolution. While competitors focus on computational photography and AI enhancement, Apple is betting that physical innovation—variable aperture, advanced optics, precision engineering—still matters to consumers willing to pay premium prices.

Xbox's strategic pivot represents the most profound shift: from hardware manufacturer to platform provider. Microsoft is betting that gaming's future lies in services and subscriptions, not console sales. If successful, this strategy could generate $20B+ in annual recurring revenue while expanding Xbox's reach to billions of gamers. If it fails, Xbox risks losing its identity and market position.

🌟 The Unifying Theme: Technology is no longer just about products—it's about strategy, agility, and understanding what customers truly value. Companies that grasp this will thrive; those that don't will struggle regardless of their technical capabilities or financial resources. The winners will be those who can balance innovation with execution, ambition with pragmatism, and vision with responsiveness to market feedback.

❓ Can Amazon Leo Actually Compete with Starlink's Massive Lead?

Competing with Starlink's 6,000+ satellite head start is daunting, but Amazon has several strategic advantages that could enable it to capture 10-15% market share by 2027. First, AWS integration creates unique value for enterprise customers—imagine edge computing nodes connected via Leo satellites, enabling real-time data processing in remote locations. Second, Amazon's $2+ trillion market cap provides patient capital to sustain losses for years while building market share. Third, the company's logistics network enables rapid customer equipment deployment at lower cost than competitors. However, Amazon faces significant challenges: Starlink's technology is more advanced (inter-satellite laser links), SpaceX controls its own launch infrastructure (lower costs, higher frequency), and the July 2026 FCC deadline creates immense pressure. Our prediction: Amazon captures 8-12% of the satellite internet market by end of 2027, primarily in enterprise and government segments, with consumer adoption lagging due to Starlink's brand strength and first-mover advantages.

❓ Why Are Institutional Investors Abandoning Bitcoin for AI Stocks?

The $2.8 billion Bitcoin ETF outflow reflects a fundamental shift in institutional risk allocation. When faced with limited risk budgets, portfolio managers are choosing AI equities over crypto for five key reasons: (1) Clear Growth Narratives—Nvidia, AMD, and other AI companies have explainable revenue growth tied to AI infrastructure buildout, while Bitcoin's value proposition remains abstract; (2) Cash Flow Generation—AI companies generate billions in profits and pay dividends, while Bitcoin produces no cash flows; (3) Regulatory Clarity—AI stocks trade on regulated exchanges with clear accounting standards, while crypto regulation remains uncertain; (4) Fiduciary Responsibility—institutional investors must justify allocations to boards and clients, and "AI infrastructure for the next computing paradigm" is easier to defend than "digital gold speculation"; (5) Higher-for-Longer Rates—with risk-free Treasury yields at 4.5-5%, the opportunity cost of holding non-yielding assets like Bitcoin is substantial. This doesn't mean Bitcoin is doomed—it means crypto needs stronger utility narratives beyond speculation to attract sustained institutional capital. The turning point will come when: (a) Fed signals rate cuts, (b) AI stock valuations become stretched, and (c) Bitcoin demonstrates clear utility in payments, DeFi, or other applications. Timeline: Q4 2026 or Q1 2027.

❓ Is Apple's Variable Aperture Camera Worth the 50% Cost Increase?

For professional photographers and serious photography enthusiasts, absolutely. Variable aperture provides precise control over depth of field and light intake that's impossible with fixed-aperture lenses, enabling DSLR-quality portrait bokeh and low-light performance. However, for average consumers who primarily take casual photos and videos, the improvement will be subtle and may not justify a $150-200 price increase. Apple's strategic rationale is threefold: (1) Pro Differentiation—creating clear separation between standard and Pro models to justify premium pricing; (2) Professional Market Expansion—targeting photographers and videographers who currently carry dedicated cameras, a market worth $5B+ annually; (3) Long-term Platform Play—this is phase one of a four-phase camera upgrade roadmap extending through 2029, creating sustained differentiation. The real question is whether consumers will pay $1,349-1,399 for iPhone 18 Pro. Our analysis suggests modest sales growth (+3-5% vs iPhone 17 Pro) as the price increase offsets feature appeal. However, the Pro Max at $1,499 will capture high-end market share from Android flagships, particularly Samsung Galaxy S27 Ultra and Google Pixel 11 Pro. Long-term, this positions Apple to dominate professional mobile photography, a niche but high-margin market segment.

❓ Why Is Xbox Delaying Project Helix and What Does It Mean for Gaming?

The Project Helix delay isn't a setback—it's a strategic choice reflecting Microsoft's transformation from console manufacturer to gaming platform provider. The company is executing a multi-year pivot toward platform-agnostic gaming where success is measured by Game Pass subscribers (target: 100M+ by 2028) rather than console sales. This strategy makes sense for several reasons: (1) Market Expansion—console gaming is ~200M users, but mobile gaming is 3B+ users; going platform-agnostic 10x's addressable market; (2) Recurring Revenue—subscription revenue is predictable and high-margin, valued by Wall Street at 5-10x higher multiples than hardware sales; (3) Content Leverage—Microsoft's $80B+ in studio acquisitions (Activision Blizzard, Bethesda) generate revenue across all platforms, not just Xbox hardware; (4) Cloud Gaming—xCloud enables Game Pass on any device, eliminating need for expensive hardware. However, this strategy carries significant risks: brand identity erosion, current console sales decline, dependency on competitor platforms, and cloud gaming technical limitations. Our prediction: Project Helix launches in late 2027 or early 2028 as "the ultimate Game Pass device"—a hybrid cloud/local gaming system priced at $399-499. By then, Game Pass will have 75-100M subscribers across all platforms, making Helix optional rather than essential. Microsoft wins by making Xbox a service, not a box.

❓ Were Google's Gemini Usage Limit Changes Sufficient?

Google's rapid response was commendable, but the changes address symptoms rather than root causes. The per-prompt cap and free failed requests are positive improvements, but the fundamental issue remains: compute-based usage limits are too complex for average users to understand and optimize. Google needs to: (1) Simplify the Model—provide clear, predictable limits that users can understand (e.g., "100 complex requests per day" rather than abstract compute units); (2) Improve Transparency—show real-time quota consumption with predictions ("at current usage, you'll hit your limit in 3 hours"); (3) Offer Flexibility—allow power users to purchase additional quota or upgrade to unlimited plans; (4) Better Education—teach users how to optimize requests to conserve quota. The competitive context is crucial: ChatGPT and Claude are aggressively courting dissatisfied Gemini users with promotional offers and simpler pricing. With 900 million monthly active users, Google cannot afford continued missteps. Our assessment: the changes are a good first step, but Google needs to iterate further based on user feedback. The company should implement a public beta program for future changes, ensuring adequate testing before full rollout. Long-term, Gemini's success depends on balancing cost control (compute limits) with user experience (predictability and simplicity)—a challenging optimization problem that Google is still solving.

📚 Sources and References

Atlas V & Amazon Leo Sources: Space.com, ULA Newsroom, Florida Today, SpaceflightNow, CNBC, Eciks.org

Bitcoin ETF Sources: CoinDesk, Decrypt, Bitcoinist, Blockchain.news, Binance, Galaxy Digital, TipRanks

Gemini Usage Limits Sources: Android Central, 9to5Google, Android Authority, WinBuzzer, Heise, Digit.in, Android Police

iPhone 18 Pro Camera Sources: MacRumors, 9to5Mac, PhoneArena, Mashable, Forbes, Apfelpatient

Xbox Project Helix Sources: GameSpot, The Verge, IGN, Windows Central, PureXbox, Shacknews

Analysis and Research: Tekin Editorial Team

🌐 Stay Connected With Us 🎮✨

For the latest tech, gaming, and gadget news, follow us on our official social media channels: